Sunil Bhandari explains everything you need to know about corporate bond finance to get that invaluable exam pass.

Corporate bond finance is the main area of debt finance that appears in the ACCA AFM exam. It regularly features within questions on cost of capital, investment appraisal, business valuations and corporate reconstructions.

This article will consider key aspects of this source of finance, focusing on the main examinable areas.

Basics

Bonds are corporate loans split into standard sizes of normally $100 and the funds are provided to the entity by many lenders. Bonds have key features including:

- They can be undated (have no maturity period, i.e. irredeemable) or more likely be redeemable.

- If the bond is redeemable, it will normally be repaid on maturity at its par value of $100. However, this could be varied by a discount or premium on the redemption value. It may even have the option to be converted into a set number of equity shares on the redemption date.

- The interest rate is set/locked when the loan is first issued on to the market. This is called the coupon rate. This is usually, but not always, set at the lender’s yield at the point of the bond issue.

- The bond will trade on the bond market at a fluid market value. In AFM this can be presented as ‘Po per $100’. This value is affected by the lenders yield as well as the number of years until maturity for a redeemable bond.

- A bond’s risk status as rated by the credit rating agencies depends heavily on the financial health of the company.

- Duration can be used to compare bonds trading on a market. This is a risk indicator for a bond. (Note that Duration ≠ Maturity but more on duration later).

Yield

The yield or yield to maturity (YTM) represents the minimum return that the lender/bondholder requires from investing in the bond. It is a value that is not fixed – it alters to reflect the changes in two factors:

- The relevant equivalent return on a government bond – risk free rate

(Rf). - The credit risk premium (CRP) as stated by the credit rating agencies.

The yield can then be used in three bond related calculations in the ACCA AFM exam to:

- Find the market value of the bond ‘Po per $100’.

- Determine the company cost of debt that is used within the cost of capital part of the syllabus.

- Estimate the duration of the bond. As mentioned, this is a risk indicator for a bond.

Also, as already stated earlier, when a bond is issued on to the market, the coupon (locked annual interest rate) will usually be set to equal the current yield.

The company issuing the bond may choose to set the coupon at a higher or lower value than the yield at the date of issue. Why would they choose to do this? The primary reason relates to future cash flow planning. The company wants to ensure it can service the debt on an annual basis and have sufficient funds to repay the bond on maturity.

The value repaid on maturity will be adjusted to reflect a lower coupon rate with a premium on redemption or even the right to convert to equity at that point. The discount on redemption offsets the higher coupon rate.

- The YTM can be computed in two ways:

- Relevant Risk-Free Rate + Credit Risk Premium (CRP)

Finding the Internal Rate of Return (IRR) of the bond cash flows – market value, interest payments and the redemption value.

The illustrations below demonstrate each of these methods.

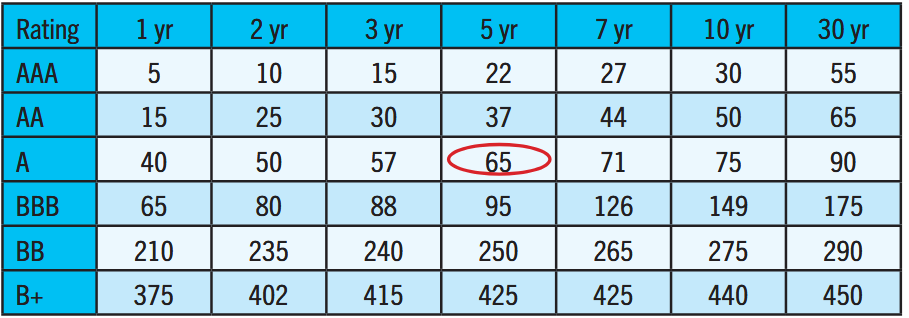

Fred Co

Table of credit spreads for industrial company bonds in basis points (0.01%) as provided by Standard and Poor’s:

The current return on five-year treasury bonds is 2.80%.

Fred Co has equivalent bonds in issue but has an A rating. YTM = Risk Free Rate + CRP = 2.80 + 0.65 = 3.45%

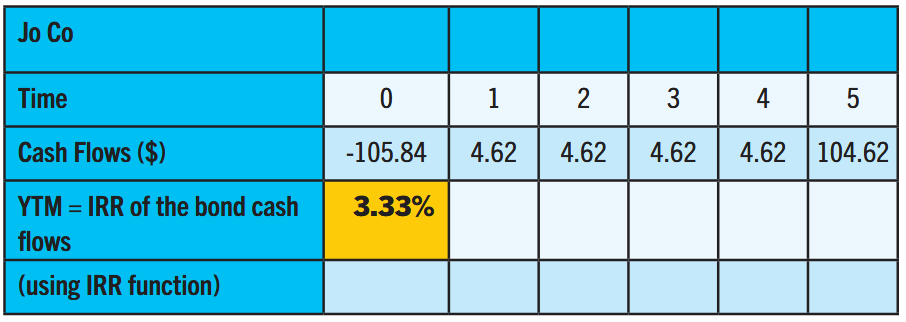

Jo Co

The company has a 4.62% bond in issue currently trading at $105.84 per $100. The bond will be redeemed at par ($100) in five years’ time.

Valuation

he valuation of corporate bonds is a very common part of ACCA AFM questions. It is particularly prevalent in questions about the cost of capital and corporate reconstruction.

Always consider the valuation of a bond from the position of the investor – the bond holder. Keep in mind that they have the minimum return they are expecting (yield). Also, they know the future cash flows they expect to receive from their investment being the coupon and the redemption proceeds.

Hence, the valuation of the bond is the present value of the future cash flows that will be received by the bond holder discounted at the minimum expected return (yield).

ACCA AFM students should be ready to deal with two styles of question:

- Using the bond’s spot yield curve rates.

- Using the bond’s yield.

Each of these are considered below.

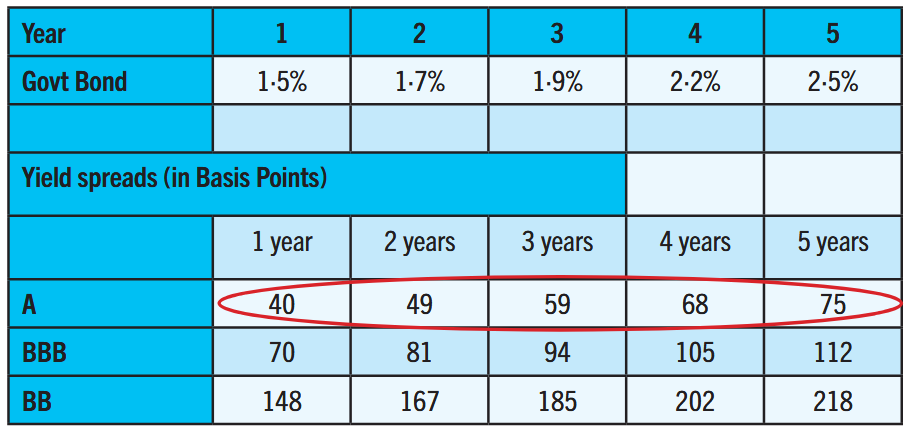

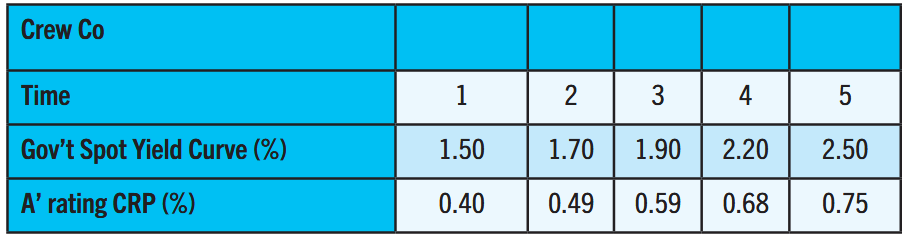

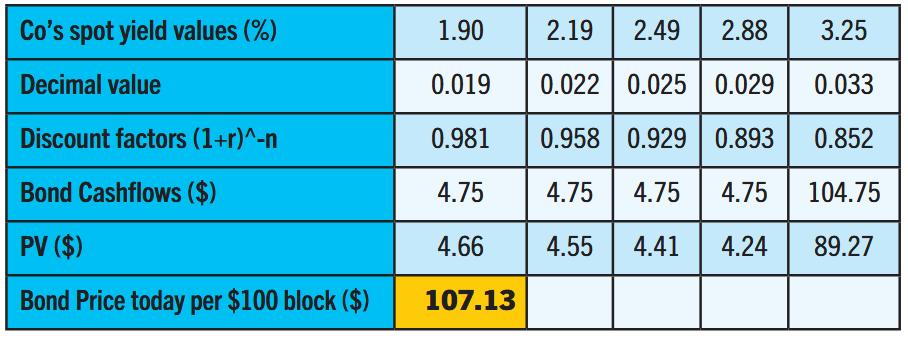

Crew Co

Crew Co currently has in issue a five-year bond with a coupon of 4.75%. It will be redeemed at par. The company has a credit rating of A.

Current government bond yield curve is as given below:

Find the current market value of the bond.

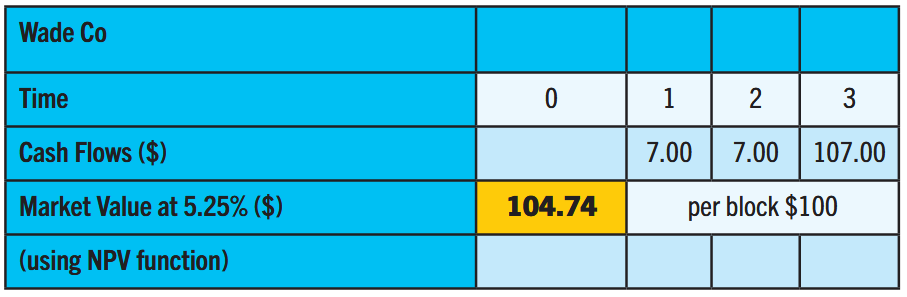

Wade Co

$20 m 7% Bond will be redeemed in three years at par ($100). Yield to maturity is 5.25%.

Duration

Bond duration is a measure of a bond’s price sensitivity to changes in interest rates, calculated as the weighted average time it takes to receive all the bond’s cash flows, including principal and interest payments.

To take a ‘keep-it-simple’ approach it is akin to the payback concept covered in ACCA FM. It’s a bit more sophisticated, but the idea is the same.

The shorter the payback the lower the risk of a project in ACCA FM.

Same here, the lower the duration the more content the bondholder feels.

There are two types of duration that can be computed:

- Macaulay Duration.

- Modified Duration.

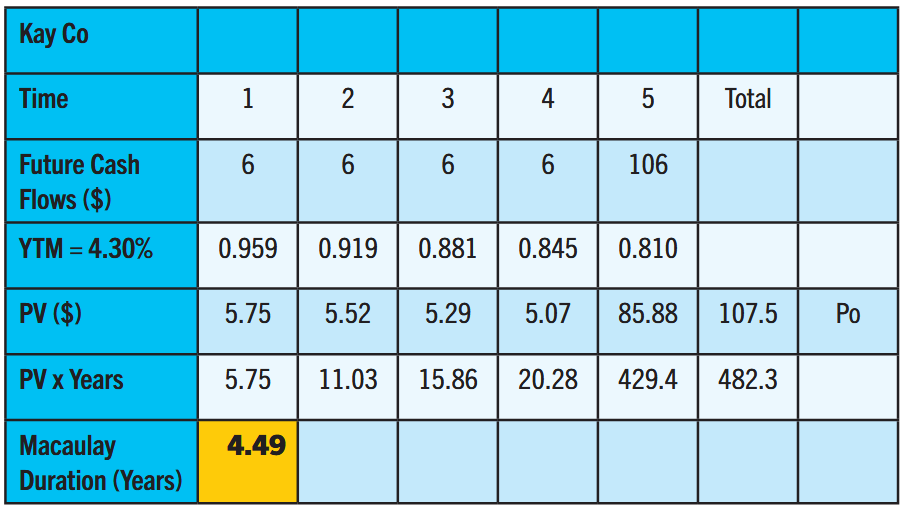

Macaulay Duration – this calculation gives each bond an overall risk weighting that allows two bonds to be compared. It is simply a composite measure of risk expressed in years.

Kay Co

Five-year 6.00% bond and the YTM (Kd) is 4.30%. Redeemed at par ($100).

Modified Duration – measured in years, modified duration is a measurement of a bond’s sensitivity to movements in interest rates. For example, a bond with a modified duration of 5.2 years can be expected to undergo a 5.2% movement in price for each 1% movement in interest rates. The longer the modified duration (in years), the more sensitive a bond’s price to changes in interest rates.

Modified Duration = Macaulay Duration / (1 + YTM)

Kay Co (once again)

Modified Duration = 4.49/ (1 + 0.0430) = 4.3 years

Conclusion

This article has considered the main examinable aspects dealing with corporate bond finance as tested in the ACCA AFM exam. It may not be as exciting as a 007 movie, but understanding the content of this article, will I believe, ensure you get more than 50% in your ACCA AFM Exam.

- Sunil Bhandari is an ACCA AFM Tutor at FME Learn Online