July 2021

In the first of a new regular column, AAT expert Teresa Clarke looks at the thorny issue of depreciation.

The accruals concept is a principle of accounting that requires the recording of expenses in the period in which they are incurred, and depreciation is an example of this. The value of a non-current asset reduces each year, mainly due to wear and tear, and this reduction is known as depreciation. We enter depreciation charges each year as a debit in the depreciation charges ledger account and as a credit in the accumulated depreciation ledger account.

Let us look at the following depreciation methods:

• Straight line

• Diminishing (reducing) balance

• Units of production

An exam task may give the following variations:

a) Depreciation is calculated on a yearly basis and charged in the year of acquisition but none in the year of disposal. This means that you enter a depreciation charge for the year in which it was purchased, regardless of when in the year the purchase took place, but no entry is made in the year the asset is disposed of.

b) Depreciation is calculated on a yearly basis and charged on a monthly basis for the months the machine is owed. This means that if the machine was purchased, or disposed of, part way through a year, you need to calculate how many months the asset was owned for in that year.

Then take the depreciation charge for the year, divide by the 12 months in the whole year and multiply by the number of months it was owned.

Straight line depreciation

For this method you need to know the cost of the asset, any residual value (the estimated selling price at the end of its life with the business) and the life of the asset.

Example: A crisp making machine in a crisp factory. The business buys a new machine to make strawberry flavour crisps and expects to make these crisps for three years only, after which the machine will be sold for scrap.

The cost of the new machine is £68,000. The useful life is three years. The scrap value of the machine at the end of the three years is £8,000.

To calculate:

Cost – residual value / years of useful life

£68,000 – £8,000 / three years = £20,000

The depreciation charge for each of the three years will be £20,000.

Diminishing (reducing) balance depreciation For this method you need to know the cost of the asset and the depreciation percentage. Any other information such as residual value is not relevant.

Example: Let us look again at the crisp factory.

The business buys a delivery van which could be used by the business for several years, so the diminishing balance method has been chosen.

The cost of the new delivery van is £24,000.

The rate of depreciation is 15% reducing balance.

To calculate:

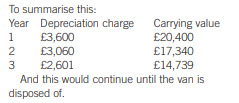

Year 1 – cost x depreciation percentage £24,000 x 15% = £3,600

Year 1 depreciation charge = £3,600

Year 2 – carrying value x depreciation percentage (£24,000 – £3,600) = £20,400 x 15% = £3,060

Year 2 depreciation charge = £3,060

Year 3 – carrying value x depreciation percentage (£20,400 – £3,060) = £17,340 x 15% = £2,601

Year 3 depreciation charge = £2,601

Units of production depreciation

For this method you will need to know the cost of the machine and how many units the machine can make before it no longer useful in the business.

Example: The crisp factory buys another machine for £35,000 to make chocolate coated crisps. The machine can make 10,000 tonnes of crisps, after which it will be disposed of for £1,000.

The business expects the following volume of crisps to be manufactured using this machine.

Year 1 – 3,000 tonnes

Year 2 – 5,000 tonnes

Year 3 – 2,000 tonnes

To calculate:

(Cost – residual value) / total units to be produced x units produced each year.

Year 1 – (£35,000 – £1,000) / 10,000 tonnes x 3,000 tonnes = £10,200

Year 2 – (£35,000 – £1,000) / 10,000 tonnes x 5,000 tonnes = £17,000

Year 3 – (£35,000 – £1,000) / 10,000 tonnes x 2,000 tonnes = £6,800

• Teresa Clarke FMAAT

If you would like to work on more depreciation tasks, you might like this workbook, which is one of my series of revision workbooks devised to support your studies. It’s called ‘Depreciation and Disposals Revision Workbook’, and is available on Amazon for £3.30 in paperback or £1.89 as an eBook. See https://www.amazon.co.uk/dp/B08X63FJH2