om Clendon tackles another subject area students frequently struggle with – impairment losses.

Question

How do you calculate and explain impairment losses?

Tom’s answer

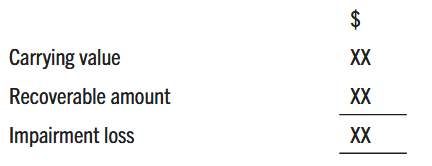

Let me dive in straight away and show you what an impairment review calculation looks like.

The carrying value is the figure that the asset is recorded at in the financial statements before the impairment review.

The recoverable amount is an estimate of how much the entity can recover from the asset. This will be the higher of what the asset could be sold for (fair value less costs to sell) and the present value of net future cash flows that the asset would generate if it were kept (the value in use).

An impairment loss arises where the carrying value exceeds the recoverable amount.

Impairment losses must be recognised and the asset written down to its recoverable amount.

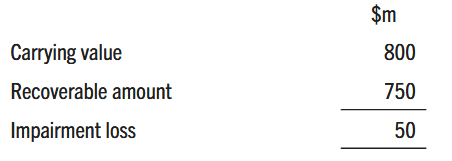

Example : impairment review

A company has an asset with a carrying amount of $800m. The asset has not been revalued. The asset is subject to an impairment review.

The fair value less costs to sell is $600m and the estimate of the present value of the future cash flows to be generated by the asset if it were kept is $750m.

Required: Calculate the impairment loss and explain the accounting treatment.

Example: Impairment review

Solution to calculation of impairment loss

Solution to explaining the accounting treatment

An asset is impaired when its carrying amount (in this case $800m) exceeds the recoverable amount. The recoverable amount is the higher of the fair value less costs to sell and the value in use. In this case, the value in use of $750m is greater than the fair value less costs to sell of only $600m. To minimise losses, in this case the asset will be kept, and the recoverable amount is therefore $750m. This means the impairment loss is $50m.

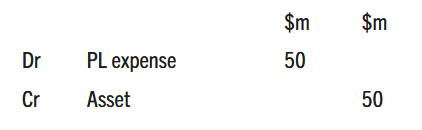

As this asset has never been revalued, the loss is charged as an expense in PL.

Impairment losses on assets that have been revalued are first charged to equity until the reserve relating to the revaluation gains of that asset is exhausted, and thereafter the impairment loss is charged as an PL expense.

The journal entry to record the impairment loss is as follows.

The additional expense will reduce the profit for the year and thus from the perspective of the statement of financial position the impairment loss reduces the retained earnings.

The impairment loss must be recorded so that the asset is written down to the recoverable amount. There is no accounting policy or choice about this. In the event that the recoverable amount had exceeded the carrying amount then there would be no impairment loss to recognise, and no accounting entry would arise.

Impairment losses are non-cash expenses, like depreciation, so in the cash flow statement they will be added back when reconciling operating profit to cash generated from operating activities.

Assets are generally subject to an impairment review only if there are indicators of impairment. Examples of circumstances that would trigger an impairment review include external sources such as a decline in market value, changes in technology and internal factors including physical damage to the asset or a worse economic performance than expected.

- Tom Clendon is a triple PQ award winning independent online tutor and podcaster who helps ACCA students pass the SBR exam. Go to www.tomclendon.co.uk or WhatsApp 07725 350793