September 2021

Sunil Bhandari explains one of the most tested subjects in the Advanced Financial Management exam – it also crops up in the Financial Management paper.

‘It’s an art, not a science’. This is a regularly used statement when introducing business valuations. This is because there are a wide range of methods that can be used to ascertain the value of the equity of a company.

Business valuations is tested in both ACCA FM and AFM. As expected, in FM the topic is introduced using basic calculations. In AFM, it is one of the most important areas of the syllabus and has been frequently examined in a far more sophisticated manner. Feel free to read my official ACCA AFM article on this topic.

The aim of this piece (and the related video) is to present the basic concepts to arrive at an equity valuation. A past FM exam question called ‘Close Co’, suitably adapted, will be used to illustrate the relevant calculations.

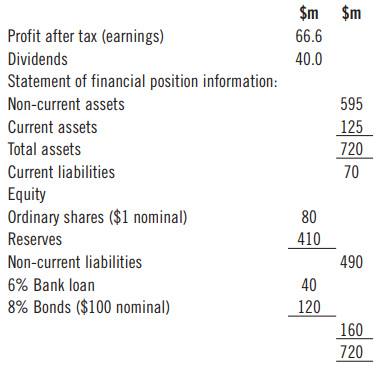

Past ACCA FM exam question (adapted) Recent financial information relating to Close Co, a stock market listed company, is as follows.

The non-current assets have a realisable value of $625m. The equivalent value for the current assets is $75m.

Financial analysts have forecast that the dividends of Close Co will grow in the future at a rate of 4% per year. The future free cash flows for the company have been estimated at $82m per year.

Close Co has a cost of equity of 10% and the WACC is 9%.

The current ex-dividend share price of the company is $8.50 per share. The industry average price-earnings ratio is 9.25.

Current Market Value

As Close Co is a listed company, this is a good starting point starting point to ascertain the value of the equity (Ve).

Hence:

Ve = Number of issued ordinary shares x current ex-dividend market price per share.

Ve = ($80m/$1) x $8.50 = $680m.

Asset Based Value

In this case, the shares are worth the value of the company’s net assets. This can be presented as a simple equation:

Ve = (Non-current assets + Current assets)

– (Non-current liabilities + Current liabilities + Preference shares)

There are three bases for valuing the net assets:

• Book value

• Net realisable value (NRV)

• Replacement cost (RC)

Using the book values:

Ve = (595+125) – (40+120+70) = $490m

Only when using the book value, the above can be circumvented to:

Ve = Issued ordinary share capital + Reserves

Ve = 80+410 = $490m

The net realisable value of the net assets is:

Ve = (625+75) – (40+120+70) = $470m

There is no information provided on the replacement cost of the net assets

Earnings Valuation

A practical and widely used valuation is take a multiple of the current earnings. The multiplier being an appropriate P/E ratio:

Ve = Current earnings x P/E ratio

Ve = $66.6m x 9.25 = $616m

Please note:

1: Dividends paid to the Preference shareholders should be deducted from earnings.

2: If no current earnings exist, a forecast future profit may be used, but this adds another degree of uncertainty to the valuation.

Dividend Valuation Model (DVM)

The dividend valuation model is also known as the dividend growth model. The equity value is equal to the present value of the future dividends discounted at the cost of equity.

This method is particularly useful when valuing a minority shareholding and hence the common presentation is to show the value on a per share (Po).

Also, if the future growth rate in the dividends is constant, the calculation is based on discounting a growing perpetuity cash flow (See my Back to Basics Financial Mathematics video).

Po = Do(1+g)/(ke -g) or Po = D1/(ke -g)

Where:

Do = the dividend per share at time 0.

D1 = the dividend per share at time 1.

g = the constant annual growth rate in the dividend per share.

ke = the cost of equity For Close Co:

Do = $40m/80m = $0.50

Po = $0.50(1+0.04)/(0.10 – 0.04) = $8.67

Ve = $8.67 x 80m = $694m

Free Cash Flow (FCF) Valuation

This method is introduced in FM, but is tested in far more detail in AFM. There are two ways to compute the equity value:

Ve = Present value of the future free cash flows for the company discounted at the WACC – market value of the debt.

OR

Ve = Present value of the future free cash flows to equity discounted at the Ke.

Given the data provided for Close Co, the former method will apply:

Ve = 82/0.09 – 160 = $751m

This assumes the book value of the debt is the same as the current market value.

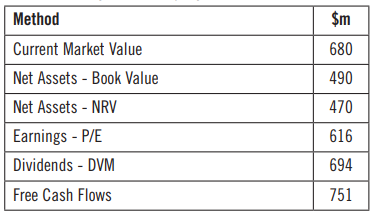

Summary and conclusion

The summary of the equity values for Close Co:

Each of the above have strengths and weaknesses, but these will be covered during your ACCA FM or AFM studies. The aim of this article was simply to demonstrate the basics behind business valuations.

• Sunil Bhandari is an ACCA FM and AFM Tutor with FME Learn Online. Go to www.SunilBhandari.com

• To check out Sunil’s Back to Basics Business Valuation video go to: https://vimeo.com/584900540.